- 4,758

- 1,409

- Joined

- Nov 6, 2012

Follow along with the video below to see how to install our site as a web app on your home screen.

Note: this_feature_currently_requires_accessing_site_using_safari

I've already been approved for the capitol one Secured card i just can't make the deposit until my first payday

And to clear up the "payday loan alternative" thing it has zero interest as long as you have the funds in your account to pay it. It's not the typical payday loan situation where you're paying like 550 for borrowing 400

From what I heard Barclay is trash all around especially their customer service and how they treat good card holders

Go with capital one

CapOne and theres no way you get denied either.

I have heard nothing but good things about the arrival plus. Didn't know they have **** customer service. You might as well get the capital one venture card. I got venture one right now since I ain't in no mood to pay yearly fees but I like it. Customer service is good imo. Also the yearly fee is cheaper on the venture card.

Both have 2%(miles per dollar) reward. At 59 a year you even out after $2,950 of spending vs the $4,450 it would take to even out with Barclays who charges 89 a year.

Thank you for the input, fellas.

I think I've read somewhere that the Barclaycard has the better redemption rate? I think it's because you get 5% of your miles back when you redeem for travel credit.

Barclaycard's customer service is really that bad?

-Drew

Never had issues with Barclays but they did close my card because I stopped using it.

yup, thats shiesty. I have a random jeweler card I got when I thought i was getting a ring with it.... year later still reporting 0 of 5kThere you have it

They aren't supposed to close your account because you don't use it. Dumbest thing ever

Applied for a credit Increase on my recently opened Amex every day card .

I haven't gotten a reponse I did it online on their site. They should I get a response within 7-10 days. Should I call?

Accounts can be closed due to long periods of no activity. Some banks are just more lenient than others.I would be heated if a company closed my account without my consent

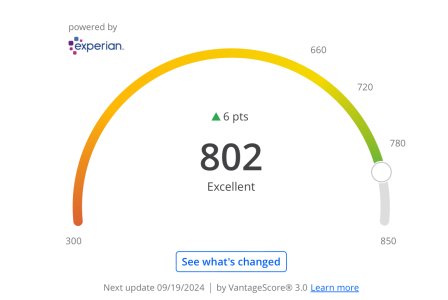

I am thinking of refinancing my auto loan as well, did your score go up because of it?I got the same response, imo they denied me.... It's cool I'm good with the 5 G, limit they gave me.... I got my auto loan refinanced a few days ago, my real Fico score is 746.... I was surprised, my interest rate dropped from 5% to 1%.... Just 6-7 yrs a go I was at 550... Now on to the 800 club

I am thinking of refinancing my auto loan as well, did your score go up because of it?I got the same response, imo they denied me.... It's cool I'm good with the 5 G, limit they gave me.... I got my auto loan refinanced a few days ago, my real Fico score is 746.... I was surprised, my interest rate dropped from 5% to 1%.... Just 6-7 yrs a go I was at 550... Now on to the 800 club

A refi won't cause your score to go up , if anything a temporary drop due to new inquiries.

I am thinking of refinancing my auto loan as well, did your score go up because of it?

When I was in college, my pops added me to his CC for emergencies or if I needed to get something. When I graduated, I decided to by myself a car. It showed that I was on the CC but didn't report it too much. Since it was the only thing on it, I had no credit history, so even though my score was a 723, I had no loan payment history and had like a 4.9% interest rate. I paid on it for a year and then refinanced it down to like 2.9% or something and dropped my monthly payment by $115.That's even better on the payday loan. You want to try and get 4-7 lines on your report whether revolving, secured, installments etc.

They don't have to be all open, but the history is nice.

I know I had several situations where kids/younger folk would come in for a loan(auto) and had 700 FICO scores, but I had banks @1.99 interest that wouldn't give them a loan because they didn't have 5 prior credit lines. All banks are different.

Just saying, the thicker the file, the better buyer you can be in a lot of situations. A Bank that's loaning money in a lot of situations, never meets you, they meet your report, and it needs to make the best impression.

There you have it

They aren't supposed to close your account because you don't use it. Dumbest thing ever

I have a Kay Jewelers card and I think after 2-3 years of inactivity they close it. I opened it in college for 1 thing and didn't use it again until I got my wife's engagement ring. I was applying for their card (they had some bonus reward dollars or something and 12 month no interest I was just going to do for the benefits and pay it off in 2-3 month chunks). They informed me that I already had a card that was just inactive. I just filled out the paperwork again and they processed it again but said that it didn't pull my credit again since I was already approved 1x. Not sure how they are doing it, but every few years I guess they do and will make it inactive but won't close it.

yup, thats shiesty. I have a random jeweler card I got when I thought i was getting a ring with it.... year later still reporting 0 of 5k

I always wondered this though.....

A refi won't cause your score to go up , if anything a temporary drop due to new inquiries.

On this link, at the top they have CC from their partners....There is a DiscoverIT card and a DiscoverIT Chrome?

Navy Federal CU credit card thread for anyone that is interested.

http://ficoforums.myfico.com/t5/Credit-Card-Applications/Official-NFCU-CLI-Guide/td-p/2101185

Currently have a 17.3K CC and 15K CLOC (Checking Line of Credit) through Navy. Many people use the CLOC for a utilization buffer.

The CLOC is pretty much overdraft protection, but you can also write checks from it.