- 33,825

- 25,392

- Joined

- Jul 13, 2005

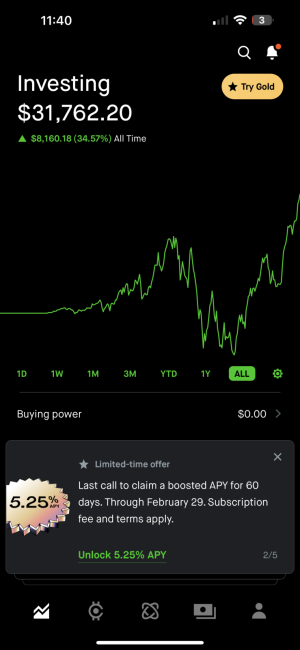

I was in the same boat as you. Once Marcus started dropping it’s savings rates, I figured it’s best to have enough in a savings account to cover mortgage/rent payments for about 6 months. The rest i moved into my brokerage account and allocated between 8-10 stocks fairly evenly.