- 4,900

- 1,145

- Joined

- Apr 12, 2011

Chase freedom givin free instant no credit hit line increases when you update your income.

O really

Follow along with the video below to see how to install our site as a web app on your home screen.

Note: this_feature_currently_requires_accessing_site_using_safari

Chase freedom givin free instant no credit hit line increases when you update your income.

Chase freedom givin free instant no credit hit line increases when you update your income.

i think its stupid that a gotdamb inquire effects us.......

Where do you do that at? Can't find it on the site anywhere haha

. On the papers that came with my card it said my score was a 746 though. Credit karma has always been around 700 . Chase declined me already so I just gotta take the L

. Chase declined me already so I just gotta take the LView media item 2092065

Going up after I got my discover card

What else can I do? Obv can't do anything about the credit length. Sign up for a new bank account or something ? I only have an ebanking and a checking account. Sign up for a savings maybe ?

I want the chase freedom unltd for that $175 but I want to take advantage of the discover IT so I'm probably not gonna get another card for a year when the "matching period" is over. Although $175 is probably more than I'm gonna get from the discover promotion. I only spend like $400-600 per month on m card so I'm gonna get like $120 back after they match it

Maybe you can answer one of my main questions I have about the age of your credit history. A lot of people say age is the most important factors when determining your credit score. They take the age of all of your accounts and average them together.If you have like capital one or amex, they give you a breakdown of your score and what factors are considered and what percent of the population has those factors. Average age of account is the highest factor and you would need at least 8 years to be in the A range as well as on time payments being the highest

Maybe you can answer one of my main questions I have about the age of your credit history. A lot of people say age is the most important factors when determining your credit score. They take the age of all of your accounts and average them together.

My question is this: How do those people who play the points game (IE they apply for cards all the time for their signup bonuses constantly) A lot of them have a really high credit score, but how is this possible? Shouldn't their age of credit history be really low if they are constantly signing up for new credit accounts? Sure you can have some cards for 12 years but if enough of your cards have an age history of 6 months 2 months 1 month etc (from signing up for new point rewards) how can age be that much of a factor?

Thanks in advance.

Letter in the mail is saying capital one platinum mastercard. And all CCs charge interest every month im assuming?Which capital one card? APR is annual percentage rate. It's the percent interest they will charge you over 12 months. So if it's 24% APR they will charge you 2% interest every month

Letter in the mail is saying capital one platinum mastercard. And all CCs charge interest every month im assuming?

Good point which is why I think I'm leaning towards discover card as my first since I'm sure its easiest to get approved and the cash back rewardsYup. A lot of cards have a zero percent interest period though for 6, 12, 18 or other months. I mean the platinum card won't earn you any rewards or anything I don't think. You can get it but if I were you I would get a card that at least gives some kind of cash back. Might as well earn money while you spend it

Good point which is why I think I'm leaning towards discover card as my first since I'm sure its easiest to get approved and the cash back rewards

Last question for today... What's apr like for the discover card?

EDIT: About to apply and see it asks for month/housing/rent payment. I currently do not pay rent for my own place yet so how would I go about this?

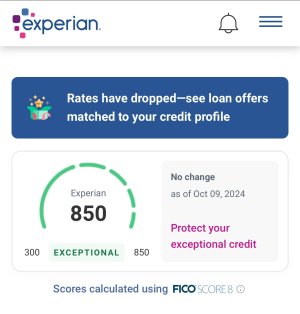

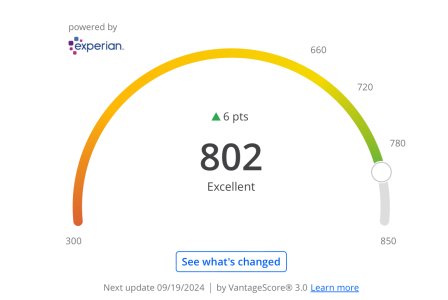

What scoring system is CITI using? My AMEX,discover, and BOA scores are always within 1-2 points of each other but my citi is always like 10-20points lower than those

I don't get these FICO scores. Last month my discover FICO was at 749. This month it's at 796. I didn't do anything major, I carry over small balances every month that are pretty much the same amount every month.