- 2,631

- 218

- Joined

- Mar 31, 2006

^If you start out with slightly below average credit (missed a few bills that went to my moms house and she never told me I had em despite opening the mail) how long till I get these type of offers.

Can someone explain to me how air miles work? Once I have money to travel again I will def grab a great air miles credit card. That one with the $99 a year charge sounds fantastic (if air miles work the way I am picturing them to)

So how do you claim them? Just say "hey i earned 15k air miles, wheres my free trip to Singapore?"

Basically think of it like this, 1 point/mile = 1 Cent.

Some points are worth more than others because of their transfer partners. The best points to earn are Citi thank you, Chase ultimate rewards, Amex membership rewards, SPG, American Airlines, etc.

Option A

You can redeem your points through the banks travel site at 1.25 cents per point. A $625 flight will cost you 50K points.

Option B

You transfer the points you've earned with your credit card to an Airline or Hotel program. This is what most people do because you can get alot more value from your points.

For example, I looked up a flight from NYC to Tokyo in December. It would cost you $2600 cash but wiith miles, it would cost 50K. This is really low so i'm assuming its low season. You'd be getting a value of 5.26 cents per point.

Sometimes It might even be better to pay for the flight to earn the miles. For example, A while ago I saw flights to Miami from NYC for $87 on AA. I have the citi prestige card which gives me 1.6 cents per point towards AA flights. The flights would of cost me about 5K points. I have platinum status with American Airlines which gives me a 100% bonus on miles flown. It's about 2200 miles to Miami and back so I would of earned 4400 miles on this trip. When you book your travel through the banks website, they treat it like a payed ticket so youre able to earn miles on it. It would of cost me only 600 miles so $6 bucks for a round trip ticket to Miami.

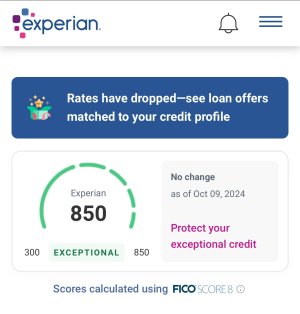

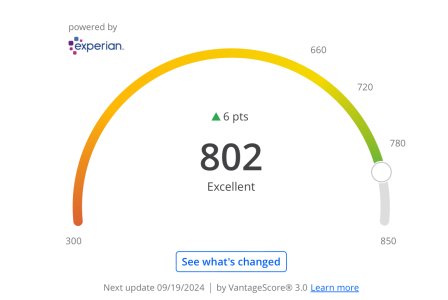

Checked my credit score...

752-764

currently have a visa thru Banana Republic

looking for a card with better rewards, what would be my options?

still fairly new to credit

I'd get the Citi premier card or Chase Sapphire preferred. Check out their bonus categories and see what works for you.

Last edited: