- 94,415

- 33,477

No pull bro

Follow along with the video below to see how to install our site as a web app on your home screen.

Note: This feature may not be available in some browsers.

I've posted about this several times throughout this thread if you want to find it. I would type it out, but I don't have time to.Can anybody offer tips or point in the right direction for dealing with COLLECTIONS. I want to pay it off asap, how does pay for deletion work?

I'm asking why you would pay it off immediately and not just wait for the statement to come in. You'll get your cashback regardless of when you pay.

It's best to pay your CC off prior to the statement.

Not for every situation. For optimal scores you should have one card report a small balance less than 10%. So pay all cards except one down to zero before the statement cuts and pay that one down to less than 10% utilization and let it report.

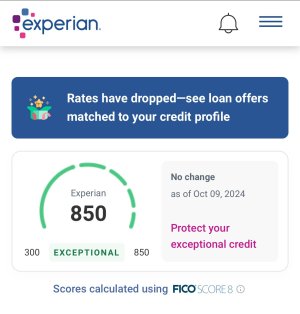

My CScore ballooned to 805 after I paid off all my CCs simultaneously, last year.

I make sure my CC's are all at 0 prior to the statement or the closing date.

But, to each is own.

My CScore ballooned to 805 after I paid off all my CCs simultaneously, last year.

I make sure my CC's are all at 0 prior to the statement or the closing date.

But, to each is own.

Your scores may have gone up after paying all of your cards but your score will be higher if you let one report a small balance. If you show zero utilization across all of your cards you show no recent credit use. Let 1% utilization report on one card one month then let all your cards report zero the next month and you will see a drop.

How much of a drop?

And is paying interest worth it?

How much of a drop?

And is paying interest worth it?

You won't pay interest unless you don't pay by your due date.

Example:

Statement cuts on May 26th. I let a $50 balance report on my card that has a $5000 limit (1% utilization). Due date is June 20th. As long as I pay that $50 before June 20th, I won't be charged any interest

Are you guys hurting that bad in the credit score department that you're micro-managing each transaction?

Are you guys hurting that bad in the credit score department that you're micro-managing each transaction?

Does that 1% utilization concept apply if its a very small balance? For example, if you have a $20 balance on a card with a $20,000 limit? Or do they round it to zero if the amount is small enough?

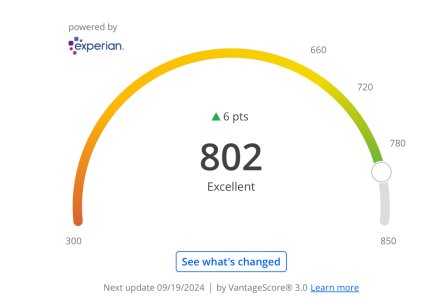

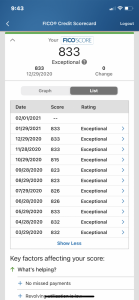

My FICO score (from Discover) is stagnating at 740-745.

lmfao im an idiot i meant 1000 it was a typo

its a hypothetical question so yeah lets just say limit is 100 and yes I pay off in full... or at least keep it under the 10% utilization rate

I've posted about this several times throughout this thread if you want to find it. I would type it out, but I don't have time to.

I should probably just save it to a Word doc to copy/paste since this comes up so often.

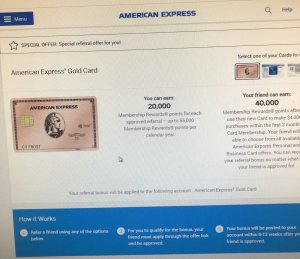

I have amex. Don't see what the hype is

AMEX has 2X points with Uber, hoping they never get rid of this. I racked up a bunch of points in Miami this weekend.

Which Amex are you guys using? I'm seeing CLI but I thought Amex basically didn't have actually limits minus their actual credit card