- Feb 11, 2008

- 19,908

- 13,198

Good info in here. Especially not relying only on the inspector and getting the HVAC, Plumbing and electrical by the respective professionals.

Follow along with the video below to see how to install our site as a web app on your home screen.

Note: This feature may not be available in some browsers.

frenchbreadbuilds I think you are confusing the HELOC with a cashout refi. A HELOC is a line of credit where the limit is based on your home equity. It does not replace your primary mortgage or the interest rate on it. You continue making payments on your mortgage as usual and you make seperate payments on the HELOC if you are carrying a balance.

It really depends on what your primary objective is. If you are looking to change residences then sell maybe as part of a 1031 exchange. If you want the best way to tap into your equity without selling then a HELOC is the way to go.sorry if I wasn’t clearer! What im directly comparing is the cost on the money I’d take out via heloc. Like is 6-8% I’d be paying on the heloc be more beneficial than just selling my home? I guess the benefit is that I still get to keep my home, which is an appreciating asset, but then I’d be paying off the heloc plus my current mortgage.

I totally understand your situation. Obviously I don't know all the details but I would suggest saving at least 5-10% down payment on cash if it's feasible. I know you mentioned houses in the 700 range or so. So I would try to save 35-70k without the heloc.sorry if I wasn’t clearer! I defintelt mixed up somethings. What im directly comparing would be cost on the money I’d take out via heloc Vs selling the house, cashing out the equity and using the proceeds as a down payment on a rental property (that we’d mortgage) and a down payment on our new house. Like is 6-8% I’d be paying on the heloc be more beneficial than just selling my home? I guess the benefit is that I still get to keep my home, which is an appreciating asset, but then I’d be paying off the heloc plus my current mortgage.

Our eventual goal is to buy a new house and we’d need to cash out on the equity in some way to have our down payment. The rental property made sense because we haven’t actually found that house yet and it would give us a place to live while we search

thinking about making a move and would for some NT folk to weigh in

so my then girlfriend/ now wife and I moved out of Philly back in 2017 and bought our first starter home in the suburbs on the Jersey side in Cherry Hill. When we paid $206k. We live in a development that consists of about 150 homes all of which are 3 variations of the same split level home. We've seen moderate rises in the comps in the neighborhood and things shot up over covid. As of last week, a home on our block that is the same model as ours sold for $410k and we are seriously considering putting our house up for sale, but the question is where do we go?

Last year we started looking at homes that wed consider our "dream home", and by looking at i mean going to open houses and hoping something sparks us to move. The issues is that all of the homes we'd be interested that have 4-5 bedrooms and 3000+sqft are $650k-$700k but require a minimum of 50-100k to update. We are starting to think that this is the new normal, which is what is it is. I think for the right house we would be willing to do it, but what do we do in the meantime? We are sitting on a bunch of equity that we want to capitalize on but a HELOC seems like an expensive way to forfeit our low interest rate. The other option is sell our current home and use some of the proceeds to make a paralell move to a condo or town house that costs a little more a month than our current mortgage. In the meantime we stash the remaining profit from our house until we find the home we want to move into permanently while keeping the town home as an investment property.

Other options are to do nothing and wait it out, or still sell our house and rent.

what do yall think?

How much does a parallel move (I assume same #br/#ba, quality, etc.) cost in your area? Moving from a 200k mortgage with 3% interest to a similar home thats now 400k at 7% in 2023 is going to eat up half of your equity to get the same monthly payment. I'd rather use that to make a dent in the dream home.

Personally, if I'm fine with my current home and didn't have a need/want for a new house (growing family, lifestyle changes, job relocating), I'd stay put. I don't have to buy a home for the sake of using my equity. Chances are I'll still have equity in 1, 2, 5 years from now when the dream home comes along my way.

If me, I'd wait it out. You're still going to have equity. You have more time to save and find a house to your liking. You don't need to deal with an additional move in a few years when you try for the next kid or find a school for your current kid.Depends where we go. Property taxes in Jersey can take huge swings in both direction. We could potentially mortgage a higher amount even at higher interest rate if we go south of the nearly $10k a year we pay in property taxes. Our family is growing too, we just had our daughter in March and plan on baby number 2 in the next few years. My wife works remotely and we gave up her home office for the nursery

It really depends on what your primary objective is. If you are looking to change residences then sell maybe as part of a 1031 exchange. If you want the best way to tap into your equity without selling then a HELOC is the way to go.

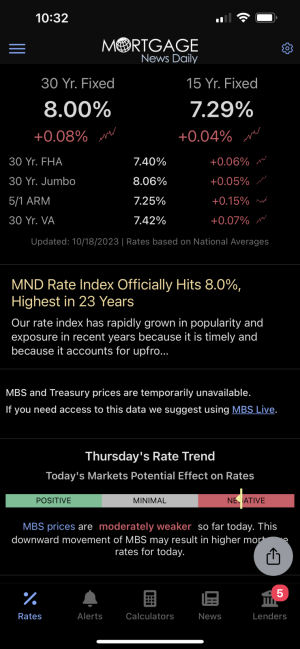

You are facing the same conundrum a lot of us pre/mid-pandemic buyers are facing: significant equity with historically low mortgage rates when prices are at all time highs.

There’s no real way to come out on top by selling in this current market unless you are moving to the middle of nowhere. Any profits are just helping you buy a more expensive - and not necessarily a bigger or better - house in both price and interest rate.

I totally understand your situation. Obviously I don't know all the details but I would suggest saving at least 5-10% down payment on cash if it's feasible. I know you mentioned houses in the 700 range or so. So I would try to save 35-70k without the heloc.

If that's not an option then check the value of the house. Get it appraised and see what your heloc options are. Most will allow you to borrow up to 80% of the value on the house (that's actually where I got my 120-150 number earlier). That should cover whatever repairs you want to do on your new house and potentially assist with the down payment. However you will now have roughly 320-350 on a mortgage (plus HELOC) on your current crib.

You could refinance the heloc into the mortgage if you choose thats probably going to be about 2700 a month (depending on taxes and insurance). Id be looking for something like 3k-3.5K a month in rent to hold onto the asset long term. If that doesn't seem reasonable for your area you could just sell. They will of course subtract the funds you owe on your mortgage as well as the funds from the HELOC. All in all you still might come out ahead. You could even use some heloc money to fix your place up and potentially get more at sale.

I just did it last year actually.If you are going to take out a HELOC, use it for something worthwhile like an investment property, don’t spend it on anything that isn’t an asset.

I’ve seen a lot of people over the years sell their current house to capitalize on the current market then make a short term move while they await their “big move” once the market corrects itself. I’ve never seen this actually work for people. Moving cost money, there are taxes, and most likely property values will continue to climb.

If you are going to take out a HELOC, use it for something worthwhile like an investment property, don’t spend it on anything that isn’t an asset.

I’ve seen a lot of people over the years sell their current house to capitalize on the current market then make a short term move while they await their “big move” once the market corrects itself. I’ve never seen this actually work for people. Moving cost money, there are taxes, and most likely property values will continue to climb.

Never would've thought of that but makes sense. We extended our patio so the turf would be about 14' away from any windows. But the backyard faces west so the turf would be exposed to a ton of afternoon/early evening sun during the summer months.Make sure you're not installing near windows... melts the turf smh. Found this out the hard way.

Not a big fan of selling in general.. the buying/selling agent usually get like 2.5% or so each, so that's -5% from your proceeds right off the bat. Closing costs another 1-2%. Then you're taxed at your income rate for any extra, most people at the 12%-22% tax brackets. Everyone uses deprecation as a tax deduction for their house, when you sell, you have to pay that deprecation you've been deducting back to the government. If you're making a huge gain, might be worth it, but I've regretted selling a few properties.The HELOC on my current home would be the down payment on my next and wed turn our current home into a rental. Initially I was talking about selling to cash out on the equity we built up, put $50k towards a condo/town home and keep the ~$150k left over for whenever we find the house we actually want to buy turning that condo into a rental in the process.

Either way we’re not waiting for the market to change necessarily. We know whatever we get into is going to cost more across the board, we’re ready for that. It’s just a matter of how our current home can be leveraged.

My turf gets full sun in Florida and is about 8 feet from any windows. Have not noticed any discoloration.Never would've thought of that but makes sense. We extended our patio so the turf would be about 14' away from any windows. But the backyard faces west so the turf would be exposed to a ton of afternoon/early evening sun during the summer months.

We were recommended wysiwash when we got our turf. We have 2 large dogs and did infill as well.Starting to get quotes for replacing the grass in the backyard with artificial turf (about 750-800 sqft total). What questions should I be asking? I also welcome any experiences with turf.

Got samples in and of course we like the most expensive, extra plush stuff (2.38" pile height). We have a dog so I'm looking into different infills to help with odor but I'm seeing spot cleaning is the best way which I'm fine with.

FL really needs to pass some laws against this. Everyone should have a fair shot at insuring their homes as long as they are in insurable condition.Thanks bro. What's weird is that I don't even have a "high risk" house. Two companies said they only insure houses built after 2003 and 2005. Mine was built in 1997. My roof was replaced in 2017 due to Hurricane Irma so it is barely 6 years old. That insurance company dropped me right after that same year.

Premium went from $1800 to $2800 to now $4400 in about a 5 year span.

Florida has Citizens insurance which is ran by the government. They offer insurance to people who get rejected by private companies. They are going to give me a quote on Monday. There are a few other smaller companies I need to check out. I'll be alright even if I stick with who I have now but the market is nuts.