- Apr 30, 2010

- 69,947

- 106,859

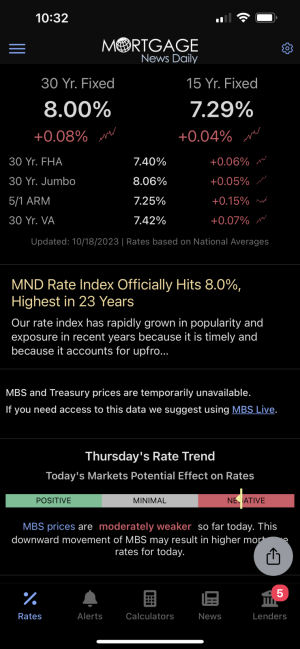

You'll owe so much over time, is it worth even buying at that rate?

Follow along with the video below to see how to install our site as a web app on your home screen.

Note: This feature may not be available in some browsers.

Prices still going up in a lot of areas despite rate hike.You'll owe so much over time, is it worth even buying at that rate?

Honestly it's killed my drive to search for investment properties.You'll owe so much over time, is it worth even buying at that rate?

Probably depends on what you consider a long time.I think you should marry the house price if you are gonna stay for a long time.. market could still take a major swing down at some point no? And in that case you’d be upside down

Or just pay cash?

GitHub needs the straight cash homie Randy Moss

Weren’t you just asking for cash handout last page?

“Time in the market beats timing the market.”I think you should marry the house price if you are gonna stay for a long time.. market could still take a major swing down at some point no? And in that case you’d be upside down

“Time in the market beats timing the market.”

For your primary residence all that matters is what you can afford to meet most of your needs. Property values can fluctuate but what does it matter if you are staying there for 5-10+ years? It takes once in a generation type events for sharp depreciation but real estate is as resilient as it gets.

There are recessions, downturns, bubbles, corrections, etc. across all markets. You can’t predict them, no one can. But it’s safe to assume markets will rebound as they always have based on 100+ years worth of data. All you can do is position yourself to take advantage of the next downswing.True for anything in investing I hear

There are recessions, downturns, bubbles, corrections, etc. across all markets. You can’t predict them, no one can. But it’s safe to assume markets will rebound as they always have based on 100+ years worth of data. All you can do is position yourself to take advantage of the next downswing.

In the meantime, if you are fortunate enough to afford a house in the current market then do it. Let go of the 2-3% rate dreams. Those aren’t coming back without another series of events to shut down the entire world, again…

Took a HELOC out. 10-year draw period requiring payments on interest only, after that starts a 20-year repayment period (interest on outstanding balance + principle). We can also pay $100 to lock (or unlock) the interest rate on however much of the balance we want. This stuff varies by bank so shop around.Can someone break down a HELOC for me?

Wife and I are thinking of moving out of our current house in the next 5-6 years and will likely use it for our down on our next place.. likely renting out this house given we have a 2.9 on it.

Is this the best route to go?

So you essentially put the dollar amount on the line you want from your equity and apply as if it’s a loan or credit line?Took a HELOC out. 10-year draw period requiring payments on interest only, after that starts a 20-year repayment period (interest on outstanding balance + principle). We can also pay $100 to lock (or unlock) the interest rate on however much of the balance we want. This stuff varies by bank so shop around.

Nothing to really breakdown beyond that. It’s just a revolving credit line. You can transfer cash to a checking account and do whatever. Or use the bank card or convenience checks issued to access funds and complete transactions.

Can’t comment on using HELOC for a second property but that is a common use. You just have to crunch the numbers on your end to compare between your other alternatives (e.g., cash on hand, liquidating porfolio/assets). Though theoretically a HELOC would be one of the “cheapest” ways to access large sums of cash because the rates will be much lower than an unsecured loan as your home is the collateral.

The credit limit on the HELOC is determined by the value of the home, the equity built, and common creditworthiness factors. I believe you can request a limit up to 80% of the equity you have. What you actually get approved for may differ.So you essentially put the dollar amount on the line you want from your equity and apply as if it’s a loan or credit line?

If I took out let’s say 80k of a heloc with today interest averages for it. How much would my monthly payment be?

www.calculator.net

www.calculator.net

place is in so cal a block from the beach too

place is in so cal a block from the beach tooI'm with United Wholesale Mortgage. They flat-out told me that they do no accept appraisals to remove PMI. She said it emphatically and repeatedly when I tried to push back on it

I went on reddit and people are saying the same thing and that lenders are refusing the appraisal route now since the appreciation was "artificial". Some people are still having success though so maybe it depends on each lender? This is BS!

I'm at $99 a month for PMI

Just gonna keep calling to see if someone else gives a different answer

How old is your loan?I'm with United Wholesale Mortgage. They flat-out told me that they do no accept appraisals to remove PMI. She said it emphatically and repeatedly when I tried to push back on it

I went on reddit and people are saying the same thing and that lenders are refusing the appraisal route now since the appreciation was "artificial". Some people are still having success though so maybe it depends on each lender? This is BS!

I'm at $99 a month for PMI

Just gonna keep calling to see if someone else gives a different answer