- 17,770

- 6,398

- Joined

- Aug 9, 2012

Congratulations dude

Follow along with the video below to see how to install our site as a web app on your home screen.

Note: this_feature_currently_requires_accessing_site_using_safari

Is it smart to pull from a 401k to use as a down payment on a house? First time home buyer in cali.

Is it smart to pull from a 401k to use as a down payment on a house? First time home buyer in cali.

Most 401ks allow you to take out a loan up to half of the 401k maxed at 50k i think. You pay the loan back to yourself and there are no penalties against you.

It really depends on the situation if it helps lower your monthly payments and you have a healthy balance in your 401k not a bad plan at all, however just remember this withdrawal will hit you tax wise when its time to file

Lastly while the payback part is true, dont forget that if you leave that job or they get acquired the money borrowed is due back for payment asap and most times you wont have that so you'll get hit with taxes.

If your looking to borrow and its sub 10k borrowing from IRA might be a better option.

What if its from a 401k from a previous job? Just sitting there and not rolled over. My co-worker was also saying something about first time buyers dont need a down payment, but under what circumstance?borrowing works a little different than an early withdraw. the main issue with borrowing is that you will get double taxed on the borrowed amount. the point of a 401k is to contribute money before tax and then you pay taxes when you withdraw (at retirement).

when you borrow from your 401k, your 401k plan will instruct your company to deduct payments from your paycheck. these payments are after tax monies. when you retire and withdraw your 401k, you will get taxed on that amount again..because to the IRS, they only see that the monies in the 401k were contributed pretax. they do not considered that you paid the borrowed amount back with taxed monies. you also need to make sure you're safe at your job because you will have to pay it back in full the moment your employment is gone.

personally, I would see if I could borrow the money from someone and pay them back with interest. Monstar mentioned the 10k and that works too. It's per person if you have a sig other/wife, it'll be 20k..assuming each person has 10k in their IRA.

What if its from a 401k from a previous job? Just sitting there and not rolled over. My co-worker was also saying something about first time buyers dont need a down payment, but under what circumstance?

anybody recently purchase their crib with an FHA loan?

How long did you research lenders? Any recommendations on where to start?

Im doing the basic google stuff and looking at multiple "FHA" information sites but I cant really judge if whatever lenders the site has partnered with is who I should really consider.

I will be looking to purchase in Houston Texas, i dont know if my location matters at all.

borrowing works a little different than an early withdraw. the main issue with borrowing is that you will get double taxed on the borrowed amount. the point of a 401k is to contribute money before tax and then you pay taxes when you withdraw (at retirement).

when you borrow from your 401k, your 401k plan will instruct your company to deduct payments from your paycheck. these payments are after tax monies. when you retire and withdraw your 401k, you will get taxed on that amount again..because to the IRS, they only see that the monies in the 401k were contributed pretax. they do not considered that you paid the borrowed amount back with taxed monies. you also need to make sure you're safe at your job because you will have to pay it back in full the moment your employment is gone.

personally, I would see if I could borrow the money from someone and pay them back with interest. Monstar mentioned the 10k and that works too. It's per person if you have a sig other/wife, it'll be 20k..assuming each person has 10k in their IRA.

401(k) loans are not taxed if they are re-paid by the borrower. However, if the loan is not repaid when you leave your employer and roll the 401(k) into an IRA, the loan amount is considered a distribution and you will owe tax on it as well as a penalty if you are under 59 ½. - Investopedia

First the loan repayments are made with after-tax income (that's once) and, second, when you take those payments out as a distribution at retirement you pay income tax on them (that's twice). ... The answer is no, you do not pay any more taxes with a 401k loan than you would on any other type of loan. Think about it.

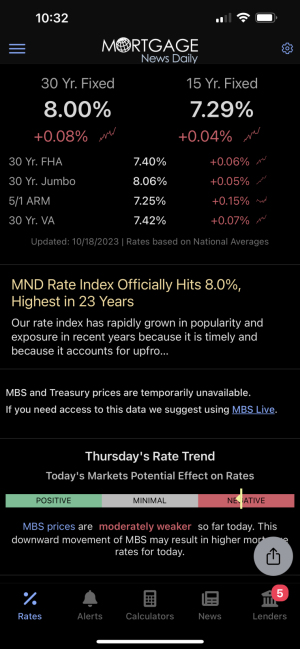

That seems pretty low for closing costs on a $600k house. Interest rate is about right on a conventional.Interest rate at 5% and 17k closing cost sound about right? House for almost 600k if it matters, 797 credit score according to credit karma also.

goddamn rates are 5% now?

I mean, rates are just going to keep going up. They aren't wrong.yea. but of course realtors will continue to insist the time to buy is now. for them its always the time to buy. their job and bonus cut depends on it. when is a realtor ever going to say its not a good time to buy lol. I see all these realtors on IG--hell anyone in the real estate business continue to say its great time to buy. i wonder what they were saying during the crash when everyone was doing short sales and forclosures.