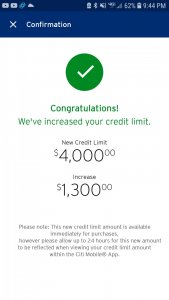

- 1,330

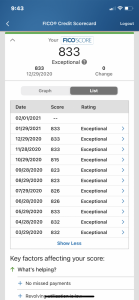

- 1,232

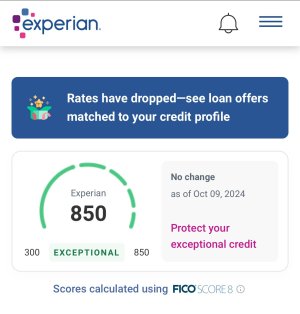

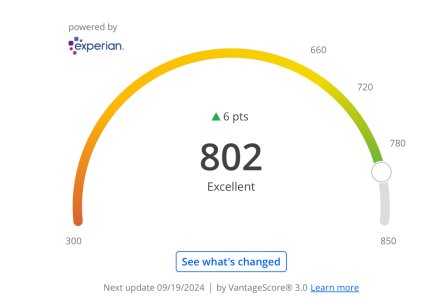

If you have more than 1 card, make sure all report $0 balance when statement cuts except for 1 which should report no more than 9%.

Follow along with the video below to see how to install our site as a web app on your home screen.

Note: This feature may not be available in some browsers.

I hear some people say keep like 10-15 in your account and let it accrue interest. Pay all in full except that $10-15. Is that good or naw?

If you have more than 1 card, make sure all report $0 balance when statement cuts except for 1 which should report no more than 9%.

wow 12 cards? what's the total credit limit

wow 12 cards? what's the total credit limit

it varies but range from 10k-15k

Nope, student loans, and the same thing applies.

I took out student loans for school.Nope, student loans, and the same thing applies.

you paid for school in cash and car?

wow props, i dunno anyone in real life who has done that..............rich family?

im not paying for my next car in cash even though i can with no problem, i don't think its a good idea personally

I took out student loans for school.

Took out a loan for my car but it was a savings secured loan. Had the cash on hand but opted to go that route for the sake of building a credit history.

Can't get cash back/miles/other perks with a lot of debit cards though.

Won't you get a better interest rate with good credit versus no credit though?

I did not. I took out student loans.Curious how did you have cash on hand for your school loans? Assuming you went immediately after high school