- 3,884

- 6,271

I'm at a 650 because of a few things I need to pay off but I should hopefully be pushing 700s by June

Follow along with the video below to see how to install our site as a web app on your home screen.

Note: This feature may not be available in some browsers.

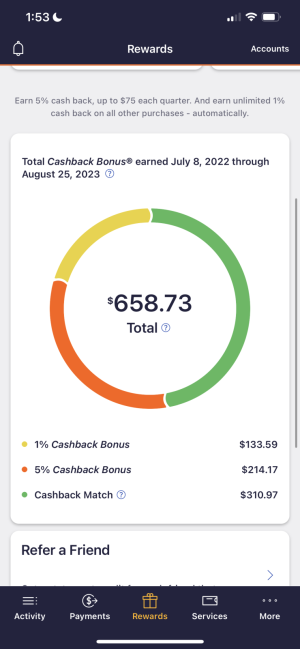

Yo, with the discover double cash back, do you also get all the referral $ you earn throughout the year doubled on your 13th statement? If so

Does anyone know the name of the that compares credit cards & basically gives you the average credit scores that get approved for each card? Trying to pick up a second card & can't remember it.

How many cards do you have now? And what were these 2 inquiries from?

should i chill on applying for cards if I have 2 recent inquiries in my history?

2 cards right now. one inquiry has to be from the recent freedom card I opened and the other...not too sure. i saw this information via this online feature capital one provides where they give you a credit score (not fico) and some other info.

How many cards do you have now? And what were these 2 inquiries from?

I think I'm at 9 or 10, I still have no issues getting approved. Mortgage shopping, car loan & refi shopping did serious damage to my inquiries lol.

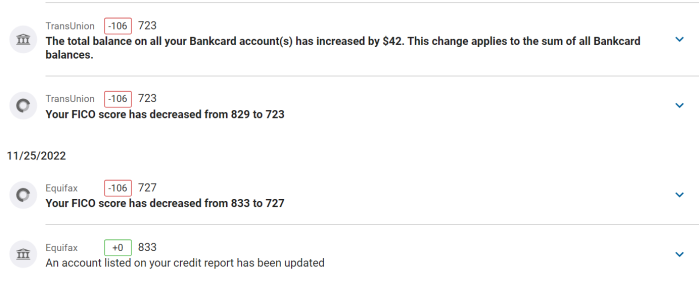

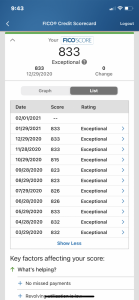

It's not so much a matter of when the credit bureaus update. It's a matter of when your lenders update their info with the credit bureaus. Generally, each company you owe money to updates with one or more of the bureaus once a month, shortly after issuing your monthly statement. If you have only one debt, then, your score will usually update once a month. If you have 10 debts, your score might update 10 times a month. Your score will also change if, for instance, you have a new hard inquiry or an old one falls off your record, or if there's a new court judgment against you, etc. In each case, the change can happen very quickly after the credit bureaus get the info. In short, your score can update as often as every day, if information comes in every day.

actually, whats the easiest/best way I can do a free credit report right now? creditkarma?

I have 17 credit cards at the moment.

Damn this thread is LIVE

800 club all over, I wonder how many ppl on NT copp Jordans and have sub prime credit score........

I found this in a Google search, my main credit card that's due on the 20th I always make sure it's under 20% utilization. My smaller one I just pay it off before due date.

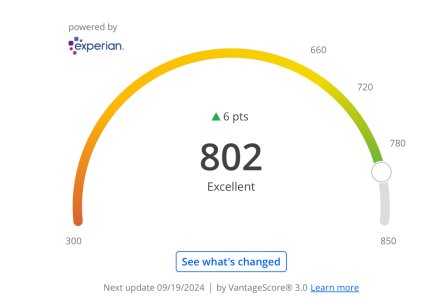

I don't even know my score right now, an I'm working on a lot of things but I will check in 45 days already started counting. This time last year I had a 740ish FICO score range. That not bad for getting good rates?

750+ gets you the best rates correct, and is there even a difference between 750 and 800 for getting loans?

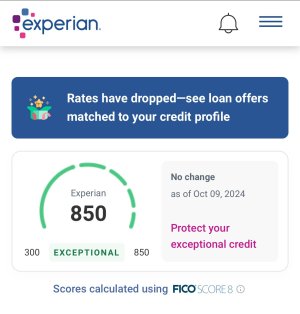

I'm 815 (at least as of last month from what barclays showed me), but I'm not sure how i got there...

")

Deciding on a travel/hotel card soon. Applied recently for the citi prestige and was denied due to lack of credit history (only 3 years or so going on 4). Thinking about getting the discover it miles card but I already have a discover it card. The only other one I have is a wells fargo cc but it sucks since the reward points expire every quarter or so and I need a certain amount to redeem.

I would like the chase sapphire or the spg card but I feel like I'll get denied for the same reason. My fico varies from 760-780 depending on my usage so I think I'm good on that part but I'm not sure if chase uses fico. I don't spend that much but when I do it's mostly for my trips so anything that multiplies points for travel, rental cars, and hotels would be nice.

Why do you need so many credit cards ?