- 1,987

- 568

- Joined

- Jul 18, 2008

I've earned almost $600 travel credit for a card I opened last sept. It's worth it.

Follow along with the video below to see how to install our site as a web app on your home screen.

Note: this_feature_currently_requires_accessing_site_using_safari

What CC do you've?I've earned almost $600 travel credit for a card I opened last sept. It's worth it.

I've earned almost $600 travel credit for a card I opened last sept. It's worth it.

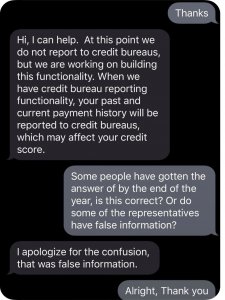

who do i contact for a collection thats appearing on my credit report thats not mine?

Barclay. Look for cards with good signup bonus.What CC do you've?I've earned almost $600 travel credit for a card I opened last sept. It's worth it.

Does it matter? It was money I was going to spend anyway. And I've have yet to spend or will spend 1cent to interest.I've earned almost $600 travel credit for a card I opened last sept. It's worth it.

How much have you spent to get that? $6000? lol

Barclay. Look for cards with good signup bonus.What CC do you've?I've earned almost $600 travel credit for a card I opened last sept. It's worth it.

Does it matter? It was money I was going to spend anyway. And I've have yet to spend or will spend 1cent to interest.I've earned almost $600 travel credit for a card I opened last sept. It's worth it.

How much have you spent to get that? $6000? lol

Whats up family wanted to see what advice others had. I have 3 cards no debt just paid them all off recently but i need to make a purchase of about 2000 ill pay that off in a couple months but i need to buy the item asap and im debating on putting all on my card and being stuck with the interest which will suck while im paying the balance on my card or if i should open a credit line at the store. Thier deal is 18 months interest free which wont take me anywhere near that long to pay, but im not gonna be using the card from the store again and i really dont want to open another card that after its balance is done i wont use again.

4. Be mindful of your bills/debts. Don't let anything ever default, or go to collections, because that will drop your credit score hard. You're a grown up, be grown up about your finances.

4. Be mindful of your bills/debts. Don't let anything ever default, or go to collections, because that will drop your credit score hard. You're a grown up, be grown up about your finances.

Yep, my credit is completely shot because of a bogus parking ticket that went to collections. It was in a private lot (a lot I used almost every day for about six months), and the ticket didn't print out of the kiosk. I contacted the company immediately to let them know I paid for the parking spot, they said it'd be fine. Got a ticket (because of course I did). I called them again, they said to provide my bank statement showing I paid for the spot. I faxed it and e-mailed a scan of it, with the ticket and my ID and everything. Got a late notice on the ticket, they told me to send all the info again, so I did. Few weeks later, I get a bill from a collections agency. That $8 parking spot has destroyed my credit. I can't even rent a car.

I've done everything in my power to maintain some semblance of a decent credit score. I pay my card off in full every month, and only once missed a payment (was out of town) and they waived it because I was in good standing (I didn't even ask them to, they offered to waive it). It's just so frustrating.

Yeah man, sometimes **** like that just sucks. You can't control it, which makes it even more infuriating because something as important as your personal credit score is in the hands of complete strangers.

Just keep working on paying off that credit card and hopefully you'll get to where you need to be. Good habits are the most important, and it sounds like you have a pretty strong foundation when it comes to financial knowledge

Besides credit cards how else can you boost your score?

I have a few hard checks and 2 credit cards and mine is only 720

What is it that you "have" to buy now?Whats up family wanted to see what advice others had. I have 3 cards no debt just paid them all off recently but i need to make a purchase of about 2000 ill pay that off in a couple months but i need to buy the item asap and im debating on putting all on my card and being stuck with the interest which will suck while im paying the balance on my card or if i should open a credit line at the store. Thier deal is 18 months interest free which wont take me anywhere near that long to pay, but im not gonna be using the card from the store again and i really dont want to open another card that after its balance is done i wont use again.

What is it that you "have" to buy now?

Yep, my credit is completely shot because of a bogus parking ticket that went to collections. It was in a private lot (a lot I used almost every day for about six months), and the ticket didn't print out of the kiosk. I contacted the company immediately to let them know I paid for the parking spot, they said it'd be fine. Got a ticket (because of course I did). I called them again, they said to provide my bank statement showing I paid for the spot. I faxed it and e-mailed a scan of it, with the ticket and my ID and everything. Got a late notice on the ticket, they told me to send all the info again, so I did. Few weeks later, I get a bill from a collections agency. That $8 parking spot has destroyed my credit. I can't even rent a car.

I've done everything in my power to maintain some semblance of a decent credit score. I pay my card off in full every month, and only once missed a payment (was out of town) and they waived it because I was in good standing (I didn't even ask them to, they offered to waive it). It's just so frustrating.

4. Be mindful of your bills/debts. Don't let anything ever default, or go to collections, because that will drop your credit score hard. You're a grown up, be grown up about your finances.

Yep, my credit is completely shot because of a bogus parking ticket that went to collections. It was in a private lot (a lot I used almost every day for about six months), and the ticket didn't print out of the kiosk. I contacted the company immediately to let them know I paid for the parking spot, they said it'd be fine. Got a ticket (because of course I did). I called them again, they said to provide my bank statement showing I paid for the spot. I faxed it and e-mailed a scan of it, with the ticket and my ID and everything. Got a late notice on the ticket, they told me to send all the info again, so I did. Few weeks later, I get a bill from a collections agency. That $8 parking spot has destroyed my credit. I can't even rent a car.

I've done everything in my power to maintain some semblance of a decent credit score. I pay my card off in full every month, and only once missed a payment (was out of town) and they waived it because I was in good standing (I didn't even ask them to, they offered to waive it). It's just so frustrating.

Yeah man, sometimes **** like that just sucks. You can't control it, which makes it even more infuriating because something as important as your personal credit score is in the hands of complete strangers.

Just keep working on paying off that credit card and hopefully you'll get to where you need to be. Good habits are the most important, and it sounds like you have a pretty strong foundation when it comes to financial knowledge

I'm 20... applied for my credit card today with bofa. I got half secured with cash rewards and a 500 dollar limit. Also no interest for 1 year

I plan on only using my CC for gas for now.. any advice?