- 4,758

- 1,409

AAoA is low, and you have a lot of inquiries in a short amount of time. Hold on to those cards for about a year. You have to build your credit it's gonna take some time .

Follow along with the video below to see how to install our site as a web app on your home screen.

Note: This feature may not be available in some browsers.

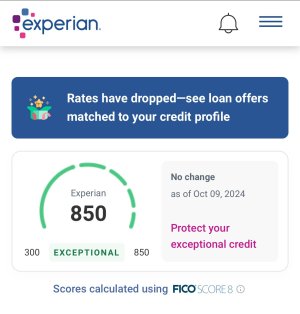

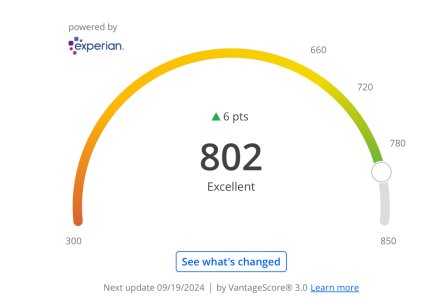

It hurts your average age of accounts, but that only accounts for 15% of your score. My scores range from 755-786. My lowest is Experian. They usually take the ding for an inquiry.

When you close an account just to take advantage of the sign up bonus how does it appear on your credit report/affect your avg age of history

already posted a few pages backBank of America now offering free Fico (TransUnion) credit score through online banking.

Yes..all approvals are based off of ur current situation..which is why they ask ur income and ur permission to pull credit..so closed accounts are good for your history..but once it is closed the only way to obtain more is applying for new cards for approvalsI read that closed accounts still show up on your report for 10 years (age of accounts wise) but the limit is removed from your total available credit after you close it. Can't confirm cause I haven't closed a card yet

Whens the best time to refinance an auto loan to get a lower apr rate?

Hey guys I'm new to this thread and I'm looking at getting a new card I already have a Discover card and want to see what you guys would recommend on getting my credit score is around 720-750 according to Credit Karma and the Fico score on the discover statements

@FreshPairs

Your whylin if you wait 6 months at 9% apr with a 792 score.

You messed up because you got your loan at the dealer, I did the same thing came out with 7.99% apr.

As soon as you get your tags refi at a credit union. My score is 100 points lower than yours and I'm sitting at 1.99%, don't wait to refi it makes no sense.

That 6 month stuff is bs, the same bs they tell you after you buy a house.

. Never get that loan at the dealer...come with your own at a CU

. Never get that loan at the dealer...come with your own at a CUWhens the best time to refinance an auto loan to get a lower apr rate?

It was actually through a credit union@FreshPairs

Your whylin if you wait 6 months at 9% apr with a 792 score.

You messed up because you got your loan at the dealer, I did the same thing came out with 7.99% apr.

As soon as you get your tags refi at a credit union. My score is 100 points lower than yours and I'm sitting at 1.99%, don't wait to refi it makes no sense.

That 6 month stuff is bs, the same bs they tell you after you buy a house.

didnt even bother trying my bank assuming my rate wouldnt get lower.

Normally CUs always give the better rate so I didnt even bother checking my bank (chase) even the dealer said i wouldnt get approved through them with only 1 line of credit (my only CC since 2007)LOL I can't believe it, they are getting over. I still wouldn't wait 6 months, as soon as it starts reporting your credit file is "thicker" due to having an installment loan.

Did you shop around or just take whatever your CU gave you?

Always remember it doesn't hurt to shop around, all CUs and banks aren't created equal and they all don't give the same rates.Normally CUs always give the better rate so I didnt even bother checking my bank (chase) even the dealer said i wouldnt get approved through them with only 1 line of credit (my only CC since 2007)

What to know about "rate shopping."

Looking for a mortgage, auto or student loan may cause multiple lenders to request your credit report, even though you are only looking for one loan. To compensate for this, FICO Scores ignore mortgage, auto, and student loan inquiries made in the 30 days prior to scoring. So, if you find a loan within 30 days, the inquiries won't affect your scores while you're rate shopping. In addition, FICO Scores look on your credit report for mortgage, auto, and student loan inquiries older than 30 days. If your FICO Scores find some, your scores will consider inquiries that fall in a typical shopping period as just one inquiry. For FICO Scores calculated from older versions of the scoring formula, this shopping period is any 14 day span. For FICO Scores calculated from the newest versions of the scoring formula, this shopping period is any 45 day span. Each lender chooses which version of the FICO scoring formula it wants the credit reporting agency to use to calculate your FICO Scores.