- 2,631

- 218

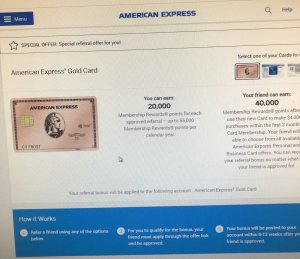

Wheres this email lol, easy 10K.

It's targeted.

Follow along with the video below to see how to install our site as a web app on your home screen.

Note: This feature may not be available in some browsers.

Wheres this email lol, easy 10K.

. I only spend like $400-600/month on my card

. I only spend like $400-600/month on my cardDo you have a Chase Freedom? I don't think the CSP is worth it unless you do. Don't know anything about the Cap One. The power in the CSP is combining points with the Freedom and transferring to partners.

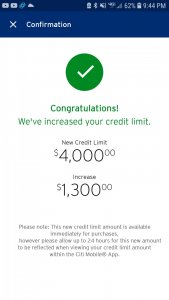

Limit of 1250... how does it work in terms of how much I use for example

I spend lets say $200 which leaves me with 1050 for the month right? So even If I pay it in full that same month I have to wait until the next statement for it to basically be at 1250 limit again?

Also with a limi of 1250 how much could I purchase I'm sure spending like $800 cant be good even if its paid in full.

If u pay it off the 1250 will b avail once ur payment clears..

I'd suggest to use it lightly at first..once u start building credit history u can request a credit increase..have u looked into getting additional cards?

Just got approved for the citi double dash. They only gave me a limit of 3k and the apr is over 20% wtf? Credit is excellent (over 800) and salary is high. Anyone else experience this when signing up for the card? Was going to use it as my new daily card, but it's not even high enough. I have a 13k limit on my freedom.

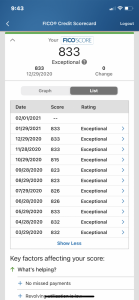

The exciting thing is my FICO is still slightly above average, so right now I qualify for home loans, but my wife and I agreed not to half-*** it and stick it out a few years to get a much nicer house and have all extra income for saving and what not as opposed to adding a house payment to all other debt -- minimal breathing room.

Got my discover it card today, love the presentation

The exciting thing is my FICO is still slightly above average, so right now I qualify for home loans, but my wife and I agreed not to half-*** it and stick it out a few years to get a much nicer house and have all extra income for saving and what not as opposed to adding a house payment to all other debt -- minimal breathing room.

Yup good luck brotha. Adding even .01% on your mortgage can have a huge affect in the overall picture, and each bit of money you save will be noticed.

That's fine, but that limit is still an issue, I already reach 2k monthly on recurring bills (rent, utilities, insurance, phone, Internet etc). This doesn't take in groceries or gas nor going out to eat, entertainment, and general spending. CL way to low for my needs to use it as my daily, which sucks because they have the max cash back points available. I would have rather just converted my other Citi card had I had known that.APRs shouldn't matter when you pay off the entire balance every month.

I just want the best perks