- 17,319

- 3,586

- Joined

- Jun 24, 2005

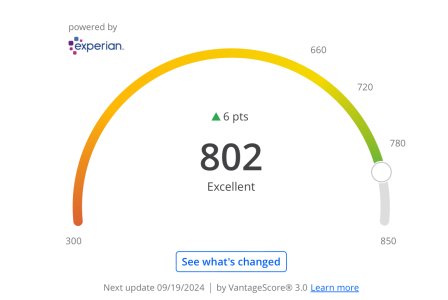

I think you worded your question wrong or are confusing a soft pull with a hard pull. Discover will do soft pulls for all CLI requests unless they tell you they need a hard pull (in that case they will contact you to get your approval before they do a hard pull). A soft pull won't show up on your credit report for others to see or impact your score.

There are times when I request a CLI and they just tell me to input how much I want to increase and my income. Once I submit, they approve it immediately.

Then, there are times when this pops up:

View media item 2018286

I'm assuming this is the "soft pull". I didn't think they did a soft pull when the limit was immediately increased upon submitting.

Will keep this in mind for the future.

Will keep this in mind for the future.