- 28,396

- 16,841

- Joined

- Mar 22, 2003

No one is driving anywhere anytime soon - no need for the new whip

Follow along with the video below to see how to install our site as a web app on your home screen.

Note: this_feature_currently_requires_accessing_site_using_safari

Yeah, I've had my accord since 2017 and i'm just going to ride with that until that electric bronco comes out. Pay like half on that car. Unless the ride share economies start hub like subscription based autonomous setups in every city to where your need for a car is tremendously less.Agreed. Unless you really NEED a new car, drive whatever you have until the wheels fall off. Just keep paying down your debt / saving / investing, and don't worry about the new car right now.

That's why the cars so affordable now tho.No one is driving anywhere anytime soon - no need for the new whip

92k miles. Just got a check engine light. I rly don't see myself keeping it past 100If your car is reliable and not giving you problems, hold on to it. Save your money.

i got the rose gold amex

its kinda girly

but i dont wanna change it back to the regular gold

cause its unique

lemme know if anyone wants the rose gold amex referral

i think u can only get a rose gold one

by a person who has one

nopeI thought the rose gold was limited edition? If you refer someone they’re probably gonna them the regular gold card.

nope

it is limited edition

but my referral link will let anyone

i refer with THAT specific link

get the rose gold

That's why the cars so affordable now tho.

92k miles. Just got a check engine light. I rly don't see myself keeping it past 100

Imma prolly 3.5k at my credit cards & see wat that do

Got a 5200 credit balance on my Capital 1

& a 2000 credit balance on my Amazon

Been @ my seasonal job for 2 months (confident they'll keep me) making $600 a week.

Got 5500 saved to cop a better whip but contemplating just holding and clearing my credit and just start saving again next month.

Any suggestions

Just turned 27 last weekSave your money for a house

Ya I got 7k 4 emergency and been meaning 2 put another rack on that, but I was waiting for Trump 2 gimme that

I'm all for riding it until it falls off except car shopping like that puts you on a timetable

Just turned 27 last week

Not tryna have kids until 30

Not getting a house until my second child

His high utilization and them reporting to the bureaus dropped his scoreOk my cousin called me asking what to do with his CC bills and I advised and hes thinking what Im saying is wrong bc my aunt said so. And I’m going to show him what other people say here if they agree with me or not.

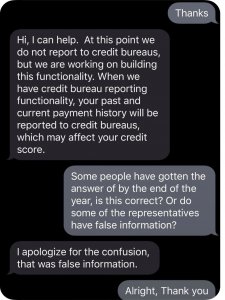

He said he has a total amt of credit avail of about 23k. He owes a total now of 10k after he paid down to zero everything but 2 cards of his. He has a cap one (owes 5500 of 6500 avail) and a citi card (4000 owed of 4800 avail). Citi reports tomorrow he says so I said pay the extra money he had to the citi. But his score dropped bc cap one reported the 85 percent utilization.

Am i wrong?

600 is considered sup prime. You will be hit with high interest ratesSo I'm about $6,000 in debt with credit cards and owe a friend money. I am barely making it paycheck to paycheck and need to get on top of my bills and pay everything down. Maybe looking at a $2,000 loan (installment loans or payday loans). My credit is closer to 600 now

I have a budget plan set up and I'm cutting out any random expenses I don't severely need.

Any advice on what the best interest rates are on specific personal loans?

Knocked out 3 credit card as a birthday present to myself last week, I could’ve got giggy wit dat $1400. I was already in the 760’s.............

His high utilization and them reporting to the bureaus dropped his score

people lie about income all the time, I have done it as wellI have a question a friend asked, that I didn't have an answer for, that maybe someone here does:

My friend has an AMEX and he has a good payment history (never late, doesn't let amounts build, etc). At the time he signed up the card, he was in college in LA, so he had no job, but they awarded him the card with a 10K limit based off his already established credit. He put his income at 30K which he told me was money he was getting from school & just other assets he calculated.

Now, he wants to raise his credit limit to improve his credit score since he will keep the same usage but the credit utilization will be where it should be since he has a higher limit, but in order to be successful at getting this he has to update his income with them, but due to the pandemic and other factors he still doesn't have a job, so he doesn't have a source of an income currently.

If he updates his income & puts something higher, will AMEX look into this? Are there ways to update credit limit without bringing up annual income with AMEX?

He doesn't want a higher limit to spend more, but just to improve his score. He's a very responsible person & not a crazy spender, but he was asking me what AMEX does when you update your income & I personally didn't know given his situation. I told him to just wait until he found a new job, but it's been about 2 years for him.

Thanks if anyone has any knowledge on how to approach this.

PO

people lie about income all the time, I have done it as well

what did he put before? I wouldn't put something crazy..

from my own experience, NOAs I said in the initial post, he told me he put $30,000. But i guess the question now is if let's say he put $50000 now (he hasn't updated that 30 since he got the card) which would help support the increase favorably, would they do anything to try to verify that?

PO