- 9,347

- 11,473

- Joined

- Aug 15, 2009

Well I tried to go for the BOA cash rewards card and got turned down, I got counter offered the secured version with a $300 deposit. Yeah...no thanks. So in the last day:

-applied for discover it: turned down for it, but got counter offered discover it with higher interest and $1000 CL

-applied for BOA cash rewards card, turned down

-applied for Capital One Venture card based off a Good approval odds with credit karma, turned down

So my rotation for credit cards is

-capital one secured platinum card: $550 CL

-discover it card: $1000 CL

-capital one quicksilver: $2000 CL

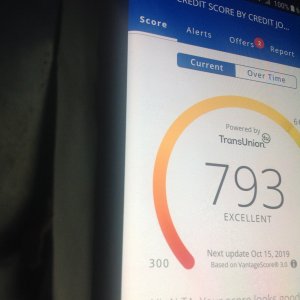

FICO 8 score is 600. I'm just going to continue to grow he'd cards for the rest of the year and chill out on any further inquiries.

-applied for discover it: turned down for it, but got counter offered discover it with higher interest and $1000 CL

-applied for BOA cash rewards card, turned down

-applied for Capital One Venture card based off a Good approval odds with credit karma, turned down

So my rotation for credit cards is

-capital one secured platinum card: $550 CL

-discover it card: $1000 CL

-capital one quicksilver: $2000 CL

FICO 8 score is 600. I'm just going to continue to grow he'd cards for the rest of the year and chill out on any further inquiries.

Last edited: