- 4,474

- 11,229

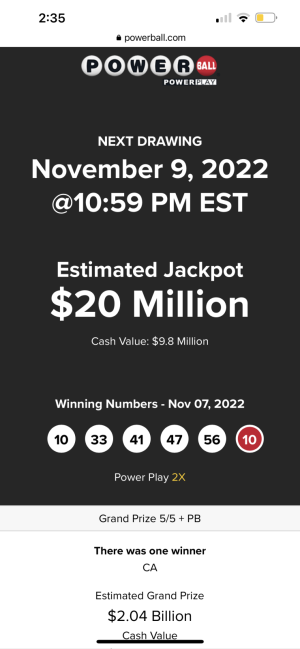

That’s wild. After taxes, the cash payout is about $240-$290 mill. You’re richer than most celebrities at that point.No winner tonight $790 million on Tuesday get your tickets

Last edited:

Follow along with the video below to see how to install our site as a web app on your home screen.

Note: This feature may not be available in some browsers.

That’s wild. After taxes, the cash payout is about $240-$290 mill. You’re richer than most celebrities at that point.No winner tonight $790 million on Tuesday get your tickets

Agreed, But, you have to be in it to win it.. All it takes is $2.Y'all just wasting money

You alright fam? Some weird stuff you spewing.I Will HaveHoly, Wise, Righteous, Phat, Nubile, Sexy, Beautiful, Gorgeous, Lovely, Loving, Loyal, Eternal, Everlasting, 12 Older & 24 Younger Wives to Help Me Serve The Almighty Lord Good God King Savior Jesus Christ Forever, Perpetually, and For All Eternity. We Will Never Have Children, We Will Live Our Entire Eternal, Everlasting Lives In Dedicated Service To The One, True, Living God from Everlasting to Everlasting. All

Where in the hell you live where 790 mill would yield you under 300?That’s wild. After taxes, the cash payout is about $240-$290 mill. You’re richer than most celebrities at that point.

Cash Value the lotto takes away 40% off the ripWhere in the hell you live where 790 mill would yield you under 300?

I'm mid 30's, I'll take an annual payment. Need all the monies.

Wonder if there's a payday lender that'll cover 800 mil...? IT'S MY MONEY AND I WANT IT NOW!

You could just put $200 million away into some safe investments and it'd most likely be worth more than $800 million after 30 years.

6% annual return would be a bit over $1 billion

That's too much money to leave on the table

Look at https://www.usamega.com/mega-millions/jackpot and https://dqydj.com/sp-500-return-calculator/ and then the time value of money to understand why you wouldn't receive the full jackpot even with the annuity payments. As suggested earlier between taxes and inflation (and risk of injury/death) you are better off taking the lump sum and investing it in dividend yielding securities. Over that same 30-yr period you could live nice off dividends and double, triple your investment or reinvest the dividends and 4-6x your money.I'm mid 30's, I'll take an annual payment. Need all the monies.

Wonder if there's a payday lender that'll cover 800 mil...? IT'S MY MONEY AND I WANT IT NOW!

Researching the numbers lead me to a comprehensive list of what do if you win the lottery (thread continued).

For simplicity let's assume you invest 100% of the annuity and lump sum. A very crude way is to calculate the present value of the annuity payouts/cash flows in comparison to the lump sum alternative. Let's use 8% as the annualized S&P500 rate of return (without dividend reinvesting) from the past 30 years which in this case will be our discount rate. Using the PV function in Excel, the annuity (17 mil every year for 30 years) discounted @ 8% is $191M. You see the PV of the annuity is almost 50% less than the $285M lump sum. If you use 10% as the discount rate which is the annualized S&P return with dividends reinvested the annuity's PV drops to $160M which is now about 80% less than the lump sum payout. Again, the jackpot number is a myth and it costs less for the lottery commission to pay you the annuity than the lump sum.Well yeah I get that, just trying to figure out what the gap would be in say investing 2/3 of the income of 510 over 30 years vs 2/3 of 296 million initially.